Historical Bond Fraud

Historical bonds are those bonds that were once valid obligations of American entities but are now worthless as securities, are quickly becoming a favorite tool of scam artists. Here are several things that you should know about them:

Types of Historical Bonds Used for Fraud

Although all sorts of historical bonds are collected and traded, historical railroad bonds comprise most of the bonds used to perpetrate fraud. Historical railroad bonds commonly used by scam artists include those issued by the Chicago, Saginaw, and Canada Railroad Co., the East Alabama and Cincinnati Railroad Co., the Mad River and Lake Erie Railroad Co., the Galveston, Houston & Henderson Railroad Co. and the Richmond, and York River Railroad Co. These railroad bonds are but a few of the 12,000 to 15,000 varieties of historical railroad bonds that are known to exist. Non-railroad historical bonds commonly used by scam artists include bonds issued by the Noonday Mining Co.

Lies Used

Lie: Historical bonds are payable in gold.

Fact: Historical bonds are not payable in gold.

Historical bonds are not valid obligations. Even if they were valid obligations, they would not be payable in gold because gold clauses in bonds issued before 1977 are unenforceable in U.S. courts. Adams v. Burlington Northern R.R. Co., 80 F.3d 1377, 1380 (9th Cir. 1996)(26K TXT file, uploaded 9/28/98); 31 U.S.C. § 5118(d)(2) (2.5K TXT file, uploaded 9/28/98).

Lie: Historical bonds are backed by the Treasury Department.

Fact: Historical bonds are not and have never been backed by us.

While historical bonds often have the words "United States of America" printed on them, these references were merely to identify the bonds as issued by entities located in the United States. Nowhere on historical bonds are there any statements that the bonds are issued or backed by us or any other part of the United States Government. Only in limited and well-known circumstances have we guaranteed obligations issued by private parties, for example, the bonds issued by the Chrysler Corporation in the early 1980s.

Lie: The Treasury Department has established a federal sinking fund to retire historical bonds.

Fact: There is no federal sinking fund to retire historical bonds.

As these historical bonds were neither issued nor backed by us or any other part of the United States Government, it would be patently absurd to suggest that we would establish a sinking fund to retire these historical bonds.

Lie: Historical bonds can be used in high-yield investment "trading program" sanctioned by any, some, or all the following entities: the International Chamber of Commerce ("ICC"), the IMF, the World Bank, the United Nations, the Federal Reserve Board, a Federal Reserve Bank, and the Treasury Department.

Fact: There are no such "trading programs," and none of these entities ever sanctions or regulates such private investment activity. For example, the IMF has issued a warning about financial schemes misusing its name.

Lie: Funds in, or some proceeds from, these high-yield trading programs go to humanitarian purposes or infrastructure development projects that are approved by the United Nations, the World Bank, or the Treasury Department.

Fact: There are no such "trading programs" or "high-yield investment programs."

The scam artist's use of humanitarian or infrastructure development theme is a trick to (1) make the investor want to believe that the trading programs are real and (2) make the investor believe that they could be helping a Third World country by forking over their money.

Lie: Historical bond trading programs yield high rates of return through the buying and selling of "debenture" or "medium term notes" supposedly issued by "prime" or "top" European or "World" banks.

Fact: Officials of leading European banks, including Barclays Bank, have denied any participation in such programs and there is no evidence that the market for such instruments exists as described by scam artists.

This appears to be a recycling of the "prime bank" schemes that have long been labeled as bogus by countless domestic and foreign banking authorities. See, for example, the warnings issued about "prime bank" scams by the Federal Reserve Board, the Federal Reserve Bank of New York and the SEC. Courts have repeatedly held that prime bank trading programs, including those purporting to generate profits through the use of historical railroad bonds, are fictitious. See, e.g., SEC v. The Infinity Group, 993 F. Supp. 324 (E.D. Pa. 1998) (prime bank instruments described as "fantasy securities")(28K TXT file, uploaded 9/28/98); SEC v. Lauer, < link to cclauer.txt> 52 F.3d 667, 670 (7th Cir. 1995) (such instruments "do not exist")(12K TXT file, uploaded 10/5/98); SEC v. Daniel E. Schneider et al., No. 98-CV-14-D (D. Wyo. February 13, 1998) (order granting preliminary injunction; "prime bank trading schemes are fictitious according to readily available information")(22K TXT file, uploaded 9/25/98).

True Values of Historical Bonds

Historical bonds are worthless as securities. None of the historical United States railroad bonds are payable by today's successor railroads such as CSX, Norfolk Southern and Union Pacific. Instead, historical bonds only have value as collector's items. A 1995 publication, Stocks and Bonds of North American Railroads: Collectors Guide with Values (one of many available publications) assessed the collector's value of the historical railroad bonds listed at between $25 and $700 each. Moreover, there are many sites on the Internet that you can visit to evaluate the collector's value of any particular bond.

Bogus Third-Party Valuations to Trick Investors

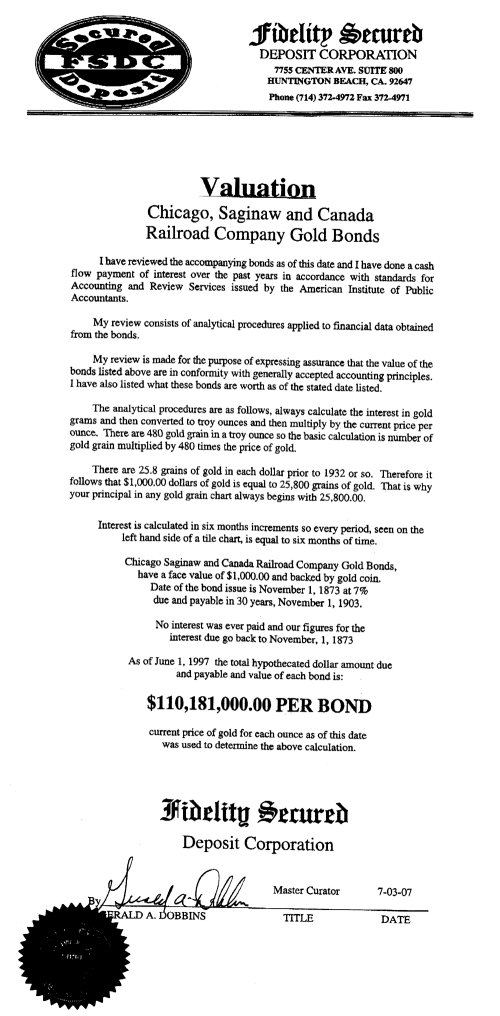

Scam artists are selling historical bonds to unsophisticated investors at inflated prices far exceeding their fair value as collectibles. They often use third-party valuations, which state that the bonds are worth millions or billions of dollars each. These valuations or authentications, which are often referred to as "hypothecated" or "hypothetical," are bogus. A typical valuation (104K JPG file, file uploaded 1/24/98) will falsely overstate the value of these bonds by assuming erroneously that, despite the unenforceability of the gold clauses contained in the bonds, and the defunct and bankrupt status of most of the bonds' issuers, some person or entity is obligated to redeem the bonds in gold bullion. See SEC v. Gerald A. Dobbins et al., No. 98-229 (C.D. Cal. May 19, 1998) (findings on order to show cause re: preliminary injunction; valuations of historical bonds held to be "misstatements")(8.5K TXT file, uploaded 9/25/98).

{kind=link}

Scam artists using such valuations may also make the false assertion that while perhaps not payable today in gold or in money, the bonds are used in high-yield trading programs in the United States, offshore and in Europe. As stated above, there are no such trading programs. In several cases, the third parties issuing the valuations appear to be working in conjunction with the scam artists. All these false assertions have been used to defraud investors into paying as much as $150,000 for historical bonds that regularly trade for $25.

Chicago, Saginaw and Canada Railroad Co. Bonds

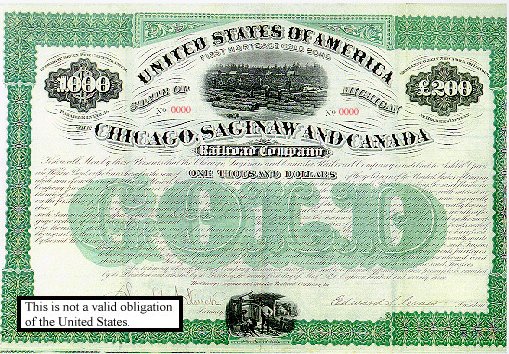

A historical bond fraud case in point involves bonds issued by the Chicago, Saginaw and Canada Railroad Co. (CS&C). It has been alleged that these securities are payable by us in gold. We neither issued these bonds, nor are they payable in gold, backed, or guaranteed by us or any other part of the United States Government. In 1873, CS&C issued 5,500 thirty-year gold-backed bearer bonds, paying seven percent interest to finance construction of a proposed railroad. Click to view a full-size image of a CS&C bond (99K JPG file, uploaded 1/24/98).

{kind=link}

CS&Cs creditors forced it into bankruptcy in 1876 and a predecessor of CSX Transportation, Inc. ("CSX") purchased its assets. CSXs predecessor did not assume any of CS&Cs outstanding debt, including the railroad bonds. All claims to money due under the bonds, which had a face value of $1,000 each, were resolved 112 years ago in the 1876 bankruptcy proceeding. At that time, investors presented their bonds for payment out of funds from the foreclosure sale and received a distribution amounting to less than 25 cents on the dollar. After the bankruptcy proceeding, the bonds remained in court archives until they were discovered in the basement of a federal building. A museum in Grand Rapids, Michigan, packaged the bonds with other historical information about this railroad for sale as collector's items for $29.95 each. Despite what a bogus valuation (104K JPG file, file uploaded 1/24/98) might claim about CS&C bonds, the bonds have no value other than as collectible memorabilia, since CSX has disclaimed any liability for redemption of these bonds, and they are most certainly not payable in gold. See Adams (26K TXT file, uploaded 9/28/98); 31 U.S.C. § 5118(d)(2) (2.5K TXT file, uploaded 9/28/98).

Courts have held that the CS&C bonds have only nominal value as collectibles. See Schneider (22K TXT file, uploaded 9/25/98) (preliminary injunction entered against defendants; bonds have "no value, except that of a collectible"). Similarly, other courts have found that bonds issued in the 1800s by the East Alabama & Cincinnati Railroad Co. and the Marietta & Northern Georgia Railway lack any investment value. See SEC v. Dobbins (C.D. Cal. March 9, 1998) (complaint)(13K TXT file, uploaded 9/25/98); SEC v. Dobbins (C.D. Cal. May 19, 1998) (8.5K TXT file, uploaded 9/25/98) (findings on order to show cause re: preliminary injunction); SEC v. Dobbins (C.D. Cal. May 19, 1998) (preliminary injunction) (7.6K TXT file, uploaded 9/25/98); Infinity Group, 993 F. Supp. at 330(28K TXT file, uploaded 9/28/98).